On April 16, the Chairman of the U.S. Commodity Futures Trading Commission publicly endorsed legislation that would break up the geographic concentration of silver depositories approved for COMEX delivery.

The mismatch between silver fundamentals and price has a structural explanation. And last month, perhaps for the first time in the history of the U.S. silver market, the regulator responsible for overseeing that structure stood up in a congressional hearing and said so.

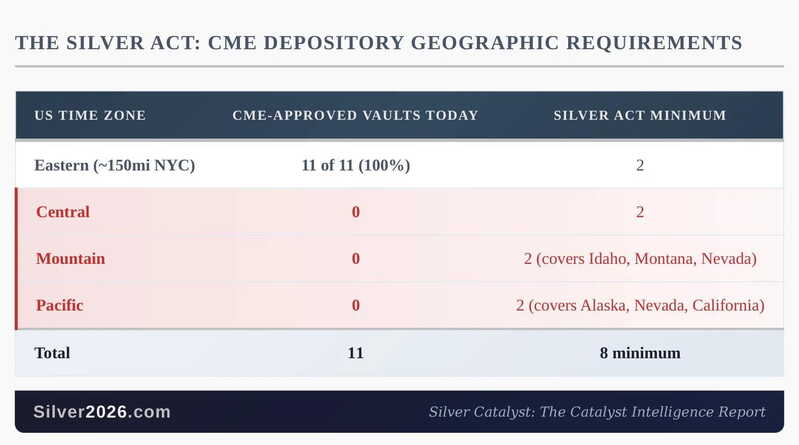

The SILVER Act and What the CFTC Chairman Said

On April 16, at a US House Agriculture Committee oversight hearing, CFTC Chairman Michael Selig publicly endorsed the System Integrity through Licensed Vault Expansion and Resilience Act (the SILVER Act), H.R. 8007, introduced March 19, 2026, by Rep. Russ Fulcher (R-ID) and Rep. Mark Harris (R-NC).

The bill’s core provision requires derivatives clearing organizations to select at least two depositories per US time zone (Eastern, Central, Mountain, Pacific) for precious metals futures delivery.

Today, every one of the 11 CME-approved gold depositories sits within roughly 150 miles of New York City. And all but one of the 12 silver depositories are within the same radius, with the one exception about 200 miles north.

The bill’s stated motivation, as articulated by Rep. Fulcher, cites “significant supply and price dislocations across the global precious metals markets over the past year.” The industry’s backing is broad, involving depositories, mints, refineries, mining companies, banks, and manufacturers. One key leader is Money Metals Depository, an independent commercial vault operating outside the New York concentration zone.

Why the Endorsement Matters More Than the Bill

The political path is uncertain. H.R. 8007 is in committee with no scheduled markup hearing. It may not advance this session.

That is secondary to what actually happened on April 16.

A Trump-appointed CFTC Chairman (the sitting head of the agency that oversees US commodity futures markets) walked into a congressional hearing and publicly aligned himself with the argument that the geographic concentration of approved silver depositories is a national security risk and a source of price dislocation. He pledged CFTC support for the legislation. The regulator suggested to Congress that the concentrated structure of the physical delivery market could be a problem.

The CFTC already has discretionary authority over depository approval criteria. The Chairman’s endorsement of the SILVER Act means that even if the bill never reaches a floor vote, the CFTC’s stance on the concentration question has been publicly stated and is now on the record. That changes the regulatory backdrop regardless of legislative outcome.

The Mechanism This Is Trying to Fix

Geographic concentration has a cost. When 100% of approved silver vaulting is clustered in one geography, the physical metal has to travel: to New York for COMEX delivery, back to London for loco London settlement, between the two during tariff scares, and ETP redemptions.

That is not an abstraction.

In January 2026, a single week saw 33.45 Moz drawn out of COMEX registered inventories, roughly a quarter of the registered pool at the time, as the tariff fear cycle forced metal from London to New York and back again.

In October 2025, the World Silver Survey 2026 documented a more serious episode. ETP allocations absorbed so much of London’s available free float that “free silver” dropped to 17% of total London inventories by end-September. One-month lease rates went from 1% to over 30% in a matter of weeks. The Survey called it a consequence of the market having “fewer degrees of freedom,” institutional language for a system with too little buffer.

Both episodes trace back to the same single-point-of-failure design: approved vaulting concentrated so tightly that a surge in demand or a shift in metal flows creates an acute, temporary shortage with no geographic safety valve.

If the SILVER Act is enacted and implemented, it will add approved vaulting in the Mountain and Pacific time zones, where most U.S. silver is actually mined. The first-order effect is logistical: shorter metal transport distances, fewer bottlenecks, and less acute exposure to single-point-of-failure settlement events.

The second-order effect is what matters more to a silver investor. When approved vaulting is geographically dispersed, the paper-physical disconnect is structurally harder to sustain. Price discovery becomes more responsive to actual supply and demand. Volatility in lease rates like October’s becomes less likely because the market operates with more degrees of freedom rather than fewer.

For an investor whose thesis depends on the six-year deficit cycle eventually showing up in price, that is a structurally bullish development. The SILVER Act does not move silver tomorrow. It addresses one of the structural reasons silver keeps misbehaving relative to its documented fundamentals.

The CFTC Chairman’s April 16 testimony is, to my knowledge, the first instance of a sitting U.S. precious-metals regulator validating that critique on the record.

Przemyslaw K. Radomski, CFA, is a precious metals investor, market analyst, and entrepreneur with over twenty years of experience focused on gold, silver, and mining stocks. A CFA charterholder, he is the founder of GoldPriceForecast dot com and SilverPriceForecast dot com, which operate within the Golden Meadow financial community, where he aims to empower individual investors with institutional-grade research.